.svg)

.png)

Every month we share our insights on relevant industry trends, resources to support founders, exclusive interviews and top news from our portfolio.

The Startups That Won't Scale or Die

In 2025, African tech startups raised $4.1 billion, a 25% rebound from the year before. A recently released 2025 Africa VC Exit and Liquidity Report, we produced with Stears, tracked 181 verified exits across fifteen years and found M&A accounting for 67 deals in 2025 alone, a 72% increase year on year. AVCA's parallel count recorded 26 VC-backed exits in 2024 with a median holding period of 3.2 years, and 63 private capital exits overall, up 47% year on year. This movement of capital and talent back into the ecosystem is a signal of an ecosystem maturing. On the surface, that sounds like good news.

Beneath the numbers was something harder to name.

More than 2,400 people were laid off across the continent's technology sector in 2025. Eighteen startups shut down entirely, publicly. Debt financing surged 63% to $1.6 billion, as founders who could no longer attract equity capital turned to the only door still open. And in portfolio review meetings that we all do as fund managers, we silently ask the same question: what do we do with the companies in the middle, the ones neither scaling nor shutting down?

I know the weight of these conversations from both sides. I have been a founder. I remember my own founder's tears (every founder has it). The morning I had to face the reality that what I had poured everything into was not going to become what I had told myself it would be. Those tears do not leave you. They shape how you see every founder who walks into a meeting holding on to the possibility that their situation is different. A lot of credit has to be given to the founders who have taken on a mandate of building something from scratch. And the reality is that it sometimes takes longer than expected to prove out the vision. And investor-founder conversations can be tough when that time is running out. It is partly why conversations like the one I am about to describe are harder to have than they look on paper.

I’ve had those conversations a few times. A lot of times with founders we have backed, and sometimes with the ones we have not. One particular pitch conversation stays with me. A founder whose company had been operating for more than four years, raised two seed extensions, but was still finding product-market fit. Nothing had gone backwards. Nothing had quite gone forward. Having seen this pattern over a few times, I immediately realized the most honest thing I could tell them was also the hardest: this company had stopped being a high growth startup and had become something else. Something that needed a different kind of capital, a different set of expectations, or an honest end.

This is the problem we are yet to find the language to address.

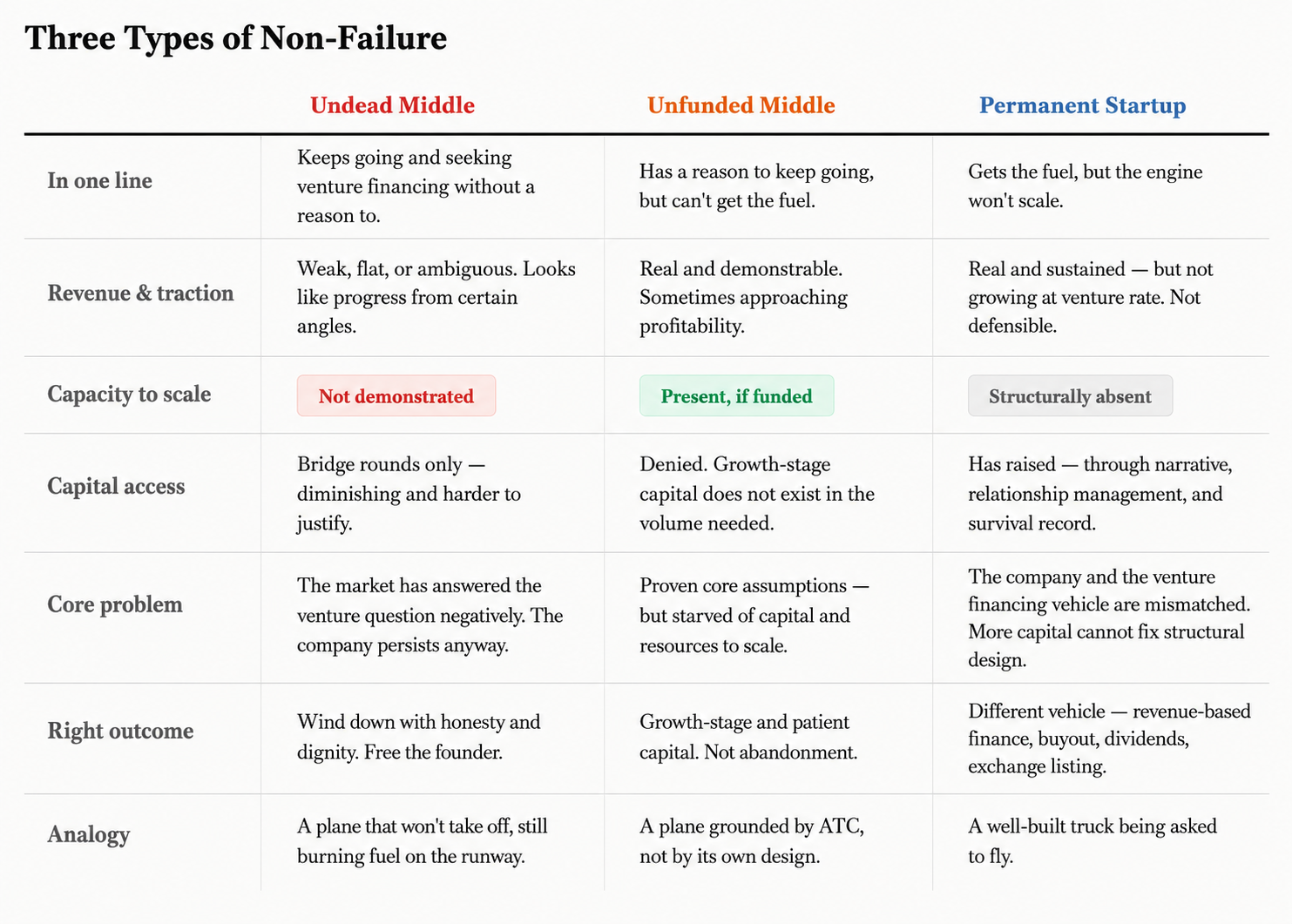

The Undead Middle

Every seed investment begins with the same premise: this company will find product-market fit, expand rapidly, and get enough traction to attract follow-on rounds. The line goes up and to the right. Someone eventually buys it. Everyone wins.

We know most do not follow that path.

A significant number of startups die at seed stage. The company tests its core assumptions rigorously, spends capital efficiently, and discovers that the market does not yet exist at venture scale, or the unit economics cannot sustain the model. Founders return remaining capital to investors, if they have not spent it all. This is not failure in any useful sense of the word. It is disciplined experimentation. The kind of scientific honesty that separates founders who come back to build stronger companies from those who carry the weight of a half-finished thing for years.

However, startup outcomes are not cleanly dichotomised between failures and winners. There are a lot of companies stuck in the non-failure middle. In my experience, companies that fall between dignified death and significant scale often resolve into three distinct patterns.

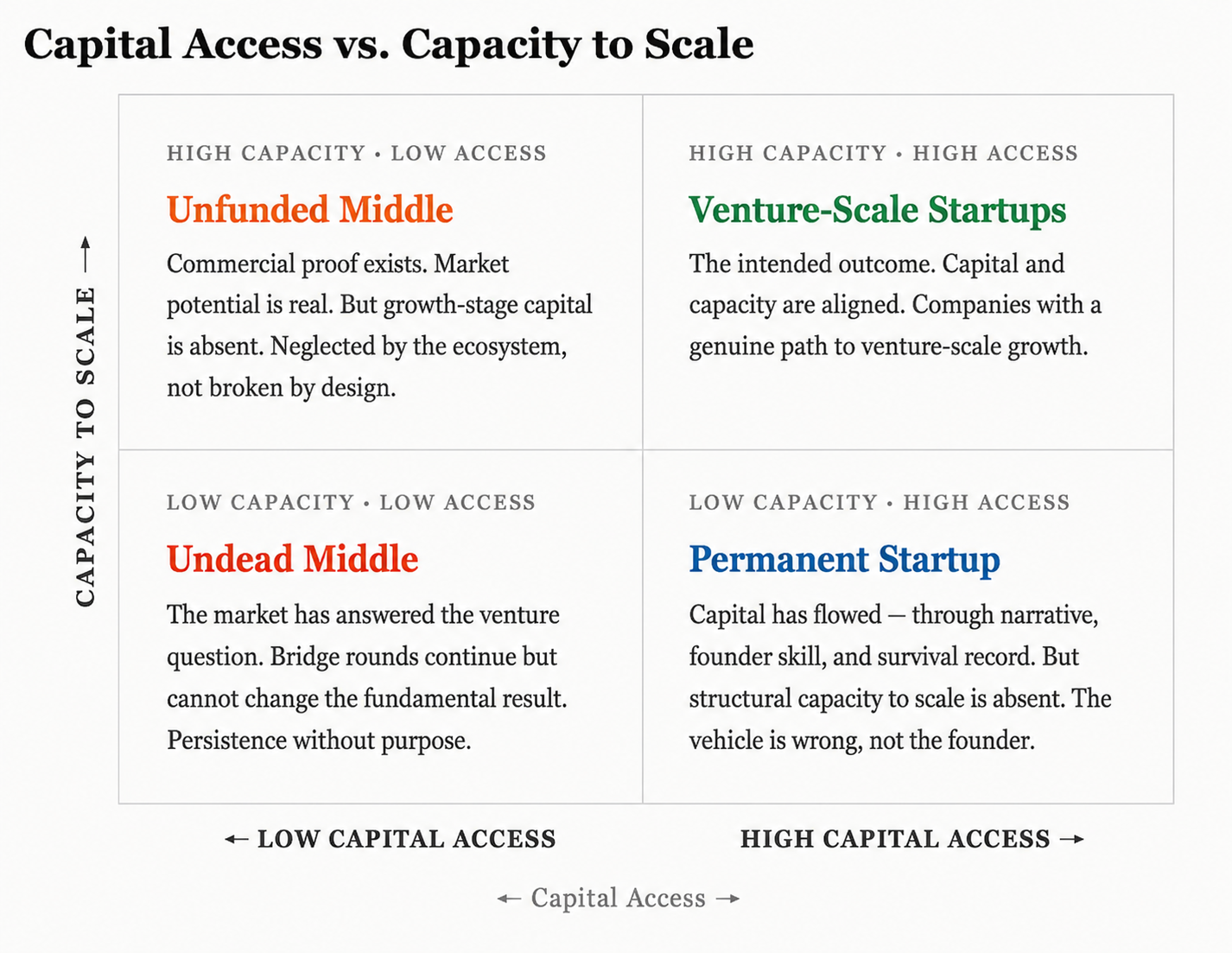

The first is companies trapped in a zombie state. The undead middle. It does not grow. It is not dead. It persists in a state of ambiguous vitality with revenues that cover some costs, traction that looks like progress from certain angles, enough activity to justify another bridge round, and not enough momentum to attract next stage capital. The markers are specific: still at seed stage four or more years after initial investment; multiple bridge extensions; flat or gradually rising revenue without a clear path to venture-scale growth; a funding round process that has started and stalled more than once without actionable feedback. This is a dangerous place to be for the founders, especially because it can be comfortable. Founders rationalise continued operation because something is working. Investors rationalise bridge rounds because there’s promise of potential growth. Venture investors are good at peddling hope. But when a startup is not flying? It persists on the runway. And this type of persistence, in venture capital, is a trap.

Undead middle companies are often not starved of capital. Some find ways to attract bridge finance, to keep the lights on, to buy another quarter. But these are companies where the market has already answered the core venture question, and more capital cannot change that answer.

It is important to state that this is not about founders quitting too early. It is about the ecosystem building honest mechanisms for sunsetting companies that have answered their core question in the negative. Especially for the sake of the founders whose time we cannot afford to waste.

The Unfunded Middle

However, there is another shape to non-failure in African startups that we do not discuss honestly. We celebrate the unicorns and the soon-icorns. We study the deaths, but we ignore the unfunded middle. The AVCA 2024 venture report documented funding concentrated at the very early stage and at capital-efficient mature companies, while a lot of post-seed, pre-Series B companies struggle to get funded. That polarisation is the financing fingerprint of a market in its early stage, where many companies get started but far fewer get the capital to reach the institutional inflection point that confirms the venture model was the right fit for them. This is not a failure of the venture model. Rather, it's a reflection of how much of the ecosystem and the financing infrastructure to support it remains to be built.

This middle is not small or anecdotal, and it is not one thing. There are companies in this category doing real revenue, solving for non-consumption in an evolving large market, sometimes approaching profitability, that still cannot raise because growth-stage capital simply does not exist in the volume the continent needs. They are not zombies. They are neglected. The distinction matters: the undead middle persists without genuine commercial proof; the unfunded middle has the proof, the revenue, the traction, sometimes a clear path to profitability, but not the capital pathway to reach its potential. The funding ecosystem has optimised for pre-seed conviction and late-stage safety and left the middle to fend for itself. That neglect creates pressure that pushes companies that could have grown into wandering undead instead. The undead middle and the unfunded middle are not the same thing. But one feeds the other.

What makes this harder to diagnose is that the exit side is moving too. Just not in the direction the headline ratio suggests. International buyers, who historically drove cash-returning exits, have declined from 56% of disclosed transactions in 2020 to 33% in 2025. What is replacing them is intra-African stock-for-stock deals. More transactions. Less cash. And a middle of the market that has nowhere to go, because they are either too pricey for other African startups to buy and too low traction to be on the radar of PE funds.

The data on delayed resolution is accumulating. TechCabal's 2025 review tracked roughly 765 disclosed job layoffs and six startup shutdowns in the first six months of the year alone. This is not in a downturn, but in the middle of a capital recovery. Headline recovery and deeper fragility are not mutually exclusive. In a market still finding its resolution mechanisms, the headline can improve while the underlying conditions that produce the unfunded middle remain intact: fragmented demand, constrained follow-on capital, mismatched company design.

The last type is the one that requires the most care to define.

The Permanent Startups

Permanent startups have survived shocks, adapted to adversity, and demonstrated genuine resilience, and yet remain structurally unchanged in their capacity to scale. They are not growing into their valuations. They are not developing the operational infrastructure that the next stage of capital would require. They sustain themselves, round after round, on the strength of a compelling narrative, a founder's ability to navigate investor relationships, and a track record of survival that the ecosystem has learned to mistake for momentum.

The distinction from the unfunded middle is important and easy to miss. The unfunded middle has earned capital but cannot access it. The permanent startup has continued to access capital, but cannot translate it into scale. One is constrained by the ecosystem's neglect. The other is constrained by fundamental design and capacity to scale (see comparison table below).

The pattern, importantly, is often structural rather than personal. In a market where roughly 80% of African startup funding originates abroad, founders must sell to investors who are several flights and multiple time zones removed from their customers. Due diligence is necessarily imperfect and requires context. The relationship between funding and value creation becomes looser than it would be in a market where capital and operations are physically proximate. Permanent startups are not simply the product of founders who have learned, sometimes inadvertently, to obscure reality; they are often the product of founders who have learned, entirely rationally, to optimise for the metrics their investors can observe from London or San Francisco rather than the operational realities that determine outcomes in Lagos or Cairo.

The ecosystem cost is real. Permanent startups occupy investor attention, absorb follow-on capital, and attract talent that could support ventures genuinely capable of transformation and scale. They create a mirage of ecosystem health, funding rounds announced, valuations maintained, but without consequential value creation or market-defining impact. In a market where capital concentration already skews heavily toward the big four and big rounds, the attention drag of misclassified companies is a measurable tax on what could actually grow.

And yet the answer is not to entirely write off the Permanent Startups. A lot of them need to exist, but they require a willingness to say that the venture model is not the right vehicle for them, and to help founders find the capital structure and ownership model that delivers genuine value for everyone. Much has been written¹, and more needs to be written, about the pathways available to companies that have outgrown the venture mould without reaching venture scale: revenue-based financing, management buyouts, secondary sales, early exchange listings, patient equity, or the underrated discipline of dividend distribution. Some of these are already happening. The ecosystem just needs to stop treating them as consolation prizes.

Trucks and Planes

The deepest insight underlying this classification - undead middle, unfunded middle and the permanent startup - is one about design. Companies are built for specific outcomes, and design mismatches cannot be solved with more capital or more time.

I often explain this with the difference between a heavy truck and a commercial aircraft. Both are designed to transport heavy loads. Both represent significant engineering investment. But a truck is designed for roads, gradients, and proximity. A plane is designed for lift, velocity, and altitude. You cannot make a truck fly by attaching wings. You cannot make an aircraft efficient by confining it to the ground.

Some companies, although tech-enabled, are designed for roads: specific communities, local optimisation, returns through persistence and consistency rather than disruptive transformation. Many of the most valuable African businesses, in distribution, trade, services, and professional infrastructure, are excellent road businesses. They serve communities that global capital has underserved. They generate returns through durability, not disruption. They deserve capital designed for their actual structure: patient, sometimes local, and aligned with cash flow rather than valuation multiples.

Tech startups, on the other hand, are designed for flight. They are fit for large, growing and yet to be defined addressable markets, favourable unit economics at scale, defensible competitive positions, unique technical depth and high intensity founders capable of reinventing organisational structure at each growth stage. When startups take too long to fly from the seed stage, they become over-engineered trucks. Stuck in the middle.

Misclassification typically emerges from unclear initial assumptions. The founder raised capital without defining, or having investors ask precisely, what success would look like, what customer acquisition cost was sustainable, what retention rate would signal genuine product-market fit, what growth trajectory would attract institutional follow-on. They encountered mixed market signals: some customers paying, some features used, some growth visible. But they could not distinguish signal from noise. A lot of the founders are not operating in bad faith. They are navigating genuine ambiguity without the analytical scaffolding to resolve it.

Trucks and planes require different revenue models, financing pathways and liquidity expectations. The distortion comes when we route venture financing into road businesses and then blame the road for not being a runway. Trucks are not designed to fly.

The Work From Here

The argument for honest classification is ultimately about time. Founder time, at an age when that time is irreplaceable. The time of the engineers and operators who joined because they believed in a mission and deserve to know whether the mission has a winnable outcome. The ecosystem time itself, which is learning, deal by deal, cohort by cohort, what kinds of companies can actually be built here, what kinds cannot but more importantly what type of capital it should allocate to the companies.

Africa's venture market has more undead and unfunded middle companies than it should. Not because its founders are weaker or its investors are less disciplined than the global peers, we are neither. But because the structural conditions make misclassification rational at every step. Smaller markets extend the search for product-market fit. Constrained follow-on capital makes the bridge round the path of least resistance. A small, densely connected ecosystem amplifies the social cost of closure far beyond its economic significance.

The conclusion is not to accelerate failure. It is to improve the quality of the decisions that determine under what condition a startup should continue. Some companies seeded by venture capital will need a different form of finance, a different exit, a different model of growth. Naming that clearly is not defeat. It is the work we need to do. The ecosystem matures not just when it produces more unicorns (we still need more), but when it gets better at building the right pathways for different types of companies.

For founders, the discipline begins at investment. Before raising and spending capital, define what success looks like, specifically, measurably, and with a timeline. What assumptions must be true for this to reach venture scale? What evidence would prove them false? How much capital is sufficient to generate that evidence? What type of capital will be needed at different stages of growth? These are not academic questions. They are the conditions under which an honest conversation about outcomes becomes possible when the market responds in ways you did not expect. And choosing a slower, smaller, more durable path is not a lesser ambition. In a market with limited funding options, it is a clearer one.

For investors, and this is me looking hard in the mirror, I recognise that my work here is both analytical and, more importantly, relational. The warning signs — metric ambiguity, milestone drift, customer distance, are often observable early, if we look for them rather than manage around them. The harder discipline is being willing to distinguish between the undead and the unfunded middle, between those two and the permanent startups, and ultimately between the trucks and the planes. And to be honest enough to confront this before the company has consumed the capital and time required for a different outcome.

The market is now forcing some of these resolutions anyway. The question is whether the ecosystem will force them with enough honesty and enough care for the people inside them to produce real learning.

—

Thanks to Oluwaseyi Tomosori, Kola Aina, Adia Sowho, Olumide Soyombo, Seni Sulyman, Anna Evi-Parker, Tayo Bamiduro, Rotimi Thomas, Damilola Teidi, Chirantan Patnaik, and Dolapo Morgan for reading providing feedbacks on drafts of this.

Notes

¹ "The Struggle to Exit: Building Scale and Liquidity in African Venture Capital" — Michelle Jideofor, Included VC. Structural diagnosis of the liquidity problem.

"From venture capital to private equity: What the new global exit trend means for African tech" — African Business (Nov 2025). The PE pathway as an alternative exit route.

"The Rise of Venture Debt in African Startups" — Lumibrief. Useful for the cautionary nuance on debt as a bridge-rather-than-exit mechanism.

Author

Dr. Dotun Olowoporoku